Building wealth isn’t just about choosing the right investments—it’s about knowing how strategy must evolve as your financial life changes. If you’re searching for clarity on how to structure your portfolio, manage leverage, and balance risk across different phases of life, this article is designed to give you practical, actionable guidance.

We break down how life stage asset allocation influences everything from capital preservation to aggressive growth strategies, and how leveraged finance and debt structuring techniques can either accelerate progress or magnify risk when misused. Whether you’re accumulating wealth, optimizing peak earning years, or protecting assets nearing retirement, understanding the mechanics behind portfolio construction is critical.

This guide draws on proven portfolio planning frameworks, high-risk investment analysis, and structured finance principles to ensure the insights are grounded in real-world financial strategy—not theory. By the end, you’ll have a clearer roadmap for aligning your investments with your goals, risk tolerance, and long-term wealth trajectory.

Your Wealth, Your Timeline

Asset allocation isn’t static; it’s a moving target shaped by careers, families, and aging parents. The idea of life stage asset allocation recognizes that your 25-year-old risk tolerance differs from your 55-year-old obligations. Still, I’ll admit forecasting markets or even your timeline isn’t precise. Experts debate optimal equity-to-debt ratios, and research can shift assumptions. That’s why a flexible, milestone-driven framework matters. Start aggressive, then gradually rebalance toward income and capital preservation as responsibilities mount (yes, even before the gray hairs). Revisit leverage, insurance, and liquidity after weddings, children, or business launches. Progress points demand portfolio shifts.

Building Your Foundation: Aggressive Growth in Your 20s and 30s

In your 20s and 30s, your primary goal is simple: maximize long-term growth. You have something Warren Buffett calls the ultimate advantage—time. With decades until retirement, market downturns are less a threat and more a temporary plot twist (think rocky training montage, not tragic ending).

Because of that runway, your risk profile can be high. That means leaning heavily into equities—stocks or stock-based funds that represent ownership in companies. A common framework is 80–90% in diversified equities (large-cap, small-cap, and international index funds or ETFs) and 10–20% in fixed income like bonds, which are loans you make to governments or corporations for steady interest.

This approach reflects life stage asset allocation, where your mix of investments aligns with your age and time horizon. Some argue this is too aggressive, especially after volatile years. Fair point. But historically, broad U.S. equities have returned about 10% annually over the long term (S&P 500 historical average, per NYU Stern data), rewarding patience.

You might also carve out 1–3% for speculative assets—venture capital funds or digital assets—using high-risk mechanics for asymmetric upside. Keep it small (pro tip: cap it so a total loss won’t derail your plan).

Next, automate contributions to your 401(k) or Roth IRA, capture employer matches, and increase your savings rate with every raise. Then ask yourself: if income grows, should your investment strategy evolve too? That’s where leverage, tax strategy, and disciplined rebalancing enter the picture.

The Accumulation Phase: Balancing Growth and Preservation in Your 40s

In your 40s, investing shifts from pure growth to strategic balance. You’re likely earning more than ever—yet expenses like mortgages, college tuition, and aging-parent support demand structure. This is where accumulation means not just building wealth, but protecting what you’ve built.

Let’s clarify a few terms. Equities are stocks, which offer growth but fluctuate in value. Fixed income includes bonds, which provide steadier returns and lower volatility (though not zero risk). Alternative assets—such as REITs (Real Estate Investment Trusts) or private credit—diversify beyond traditional stock and bond markets.

Finding the Right Balance

A moderate-to-high risk profile typically fits this decade. In practice, that often means:

- 65–75% equities to outpace inflation (which has averaged about 3% annually long term, per U.S. Bureau of Labor Statistics data).

- 25–35% fixed income to reduce portfolio swings.

- A measured allocation to alternatives for diversification.

This approach reflects life stage asset allocation—adjusting investments according to your age and financial responsibilities.

However, some argue you should stay aggressively invested in stocks to maximize returns. After all, retirement may still be 20+ years away. That’s fair. Historically, equities have outperformed bonds over long periods (S&P 500 long-term annualized return ~10%, per S&P Global). Still, sequence-of-returns risk—the danger of major losses right before retirement—makes reducing volatility prudent.

Equally important is debt strategy. Max out retirement accounts first. Then evaluate high-interest debt versus liquidity tools. In some cases, a portfolio-backed line of credit can provide flexibility without triggering taxable asset sales (pro tip: compare interest costs carefully).

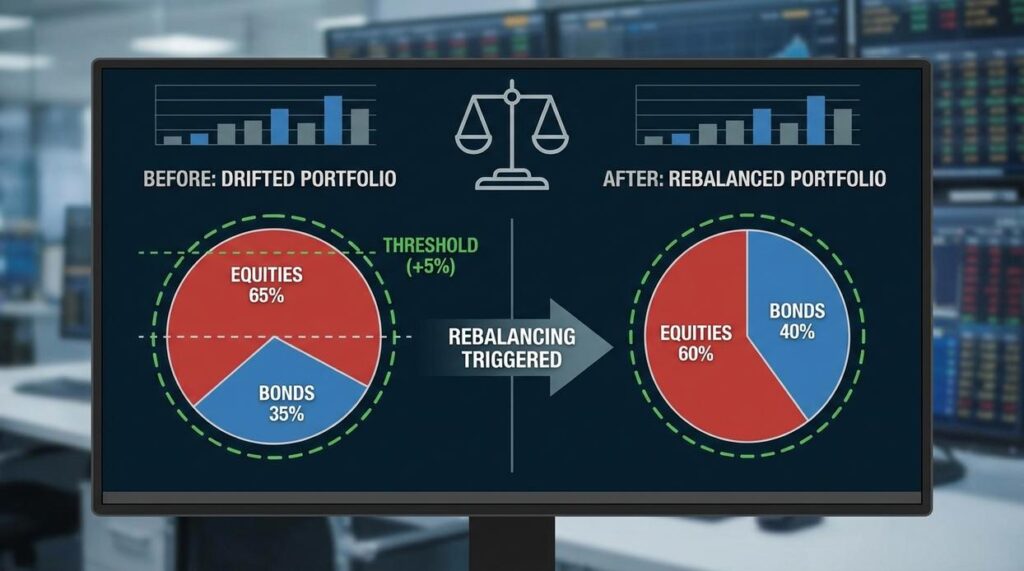

If you’re unsure about allocations, review how to rebalance your portfolio for long term stability: https://roarleveraging.com.co/how-to-rebalance-your-portfolio-for-long-term-stability/

In your 40s, the goal isn’t chasing every rally—it’s building resilience.

The Preservation Phase: Fortifying Your Portfolio in Your 50s and Early 60s

This is the stage where the game changes. You’re no longer sprinting toward growth—you’re protecting what you’ve built (because a major drawdown at 62 hits differently than one at 32).

The primary goal is simple: preserve capital and generate dependable income. That means shifting from aggressive accumulation to disciplined defense. In life stage asset allocation, this is where portfolios often move toward a 40–50% equity and 50–60% fixed income mix, emphasizing stability over upside.

Some investors argue you should stay heavily in stocks to outpace inflation. Historically, equities have returned about 10% annually over the long term (S&P 500 historical averages, NYU Stern data). Fair point. But sequence-of-returns risk—the danger of poor market performance just before or after retirement—can permanently impair withdrawals (Morningstar research). Preservation reduces that threat.

Sample Allocation Focus:

- High-quality, dividend-paying stocks

- Government and investment-grade corporate bonds across varied durations

- Cash equivalents for liquidity

Build at least one year of living expenses in cash. Rebalance annually. Model retirement income needs conservatively (pro tip: stress-test for a 20% market drop).

Competitors often stop at “shift conservative.” The real edge? Integrating bond duration strategy with withdrawal timing—so income aligns with spending waves, not just market cycles.

The Distribution Phase: Making Your Wealth Last in Retirement

The distribution phase is when your portfolio shifts from accumulation to income production. In simple terms, you’re no longer building the engine—you’re living off its fuel. The goal is sustainability: generating income while protecting principal from inflation (the steady rise in living costs) and longevity risk (outliving your savings).

Life stage asset allocation matters most here. Compare two approaches:

- Growth-Heavy (60%+ equities) – Higher upside, but sharper volatility. A bad sequence of returns early in retirement can permanently reduce income.

- Balanced Distribution (30–40% equities, 60–70% income assets) – More stability through bonds, annuities, and Treasury Inflation-Protected Securities (TIPS), which adjust with inflation (U.S. Treasury).

Some argue keeping stocks high beats inflation long term. Historically, equities have returned about 10% annually before inflation (S&P Global). True—but retirees don’t have decades to recover from deep drawdowns. Preservation now outranks maximization.

Key actions include:

- Implementing a systematic withdrawal plan like the 4% rule (Bengen, 1994) or dynamic withdrawals.

- Managing Required Minimum Distributions (RMDs) to reduce tax drag (IRS).

- Reviewing the plan every 2–3 years.

Think of it like switching from offense to defense in the fourth quarter—you’re playing to win, but mostly to avoid losing.

Your financial journey is unique, yet too many portfolios sit untouched for years. Nothing is more frustrating than realizing your investments no longer match your reality. Maybe you’re taking big risks in your 60s, or playing it safe in your 20s. That’s not strategy; it’s neglect.

Life demands alignment.

A smart life stage asset allocation approach treats your portfolio as a living plan that evolves with each progress point. Instead of drifting, you intentionally adjust:

- Reduce exposure as retirement nears

- Increase growth assets when time is on your side

- Rebalance after major milestones

This framework eliminates guesswork and prevents pain.

Take Control of Your Financial Leverage Today

You came here to better understand how leveraged finance, debt structuring, and portfolio strategy can accelerate—or undermine—your wealth building goals. Now you have a clearer picture of how progress points, risk exposure, and life stage asset allocation work together to shape long-term outcomes.

The reality is this: unmanaged leverage and poorly structured debt can quietly erode your gains and magnify losses. High-risk investment mechanics are powerful, but without a disciplined framework, they can stall your financial progress instead of advancing it.

The opportunity is in applying what you’ve learned. Align your leverage with your current life stage. Stress-test your portfolio. Reevaluate your debt structure. Make sure every dollar you borrow or deploy has a defined purpose and measurable upside.

If you’re serious about optimizing returns while controlling downside risk, now is the time to act. Get a structured leverage review, refine your portfolio positioning, and implement a strategy built to withstand volatility. Proven frameworks, data-driven insights, and disciplined allocation methods make the difference between reactive investing and strategic wealth building.

Don’t let misaligned leverage hold you back. Take the next step today and position your portfolio for smarter, stronger growth.

Ask Elveris Xelthanna how they got into wealth portfolio planning and you'll probably get a longer answer than you expected. The short version: Elveris started doing it, got genuinely hooked, and at some point realized they had accumulated enough hard-won knowledge that it would be a waste not to share it. So they started writing.

What makes Elveris worth reading is that they skips the obvious stuff. Nobody needs another surface-level take on Wealth Portfolio Planning, Progress Points, High-Risk Investment Mechanics. What readers actually want is the nuance — the part that only becomes clear after you've made a few mistakes and figured out why. That's the territory Elveris operates in. The writing is direct, occasionally blunt, and always built around what's actually true rather than what sounds good in an article. They has little patience for filler, which means they's pieces tend to be denser with real information than the average post on the same subject.

Elveris doesn't write to impress anyone. They writes because they has things to say that they genuinely thinks people should hear. That motivation — basic as it sounds — produces something noticeably different from content written for clicks or word count. Readers pick up on it. The comments on Elveris's work tend to reflect that.

Ask Elveris Xelthanna how they got into wealth portfolio planning and you'll probably get a longer answer than you expected. The short version: Elveris started doing it, got genuinely hooked, and at some point realized they had accumulated enough hard-won knowledge that it would be a waste not to share it. So they started writing.

What makes Elveris worth reading is that they skips the obvious stuff. Nobody needs another surface-level take on Wealth Portfolio Planning, Progress Points, High-Risk Investment Mechanics. What readers actually want is the nuance — the part that only becomes clear after you've made a few mistakes and figured out why. That's the territory Elveris operates in. The writing is direct, occasionally blunt, and always built around what's actually true rather than what sounds good in an article. They has little patience for filler, which means they's pieces tend to be denser with real information than the average post on the same subject.

Elveris doesn't write to impress anyone. They writes because they has things to say that they genuinely thinks people should hear. That motivation — basic as it sounds — produces something noticeably different from content written for clicks or word count. Readers pick up on it. The comments on Elveris's work tend to reflect that.