Building a resilient financial future requires more than chasing returns—it demands a clear understanding of leverage, risk exposure, and strategic capital allocation. If you’re searching for practical insights on progress points, leveraged finance, debt structuring, and high-risk investment mechanics, this article is designed to give you exactly that. We break down how sophisticated investors approach borrowing, manage volatility, and structure positions to strengthen a diversified investment portfolio without losing sight of downside protection.

Many investors struggle to balance growth ambitions with risk control, especially when leverage and complex instruments enter the equation. Here, you’ll find clear explanations, strategic frameworks, and real-world applications that translate advanced financial concepts into actionable guidance.

Our insights are grounded in deep analysis of market structures, portfolio strategy research, and proven wealth-planning methodologies. By the end, you’ll understand how to evaluate leverage responsibly, structure debt effectively, and position your capital with greater confidence and clarity.

The Architectural Blueprint for a Resilient Portfolio

Think of wealth building as architecture. Option A: a single towering pillar—say, all stocks. Option B: multiple load‑bearing beams across assets. When storms hit (and markets always storm), which structure stands?

A diversified investment portfolio spreads capital across equities, bonds, real assets, and alternatives to reduce concentration risk—meaning the danger of one failure collapsing everything (Investopedia). Critics argue concentration builds faster wealth. True—when you’re right. But history shows single-asset exposure magnifies drawdowns, as seen in the 2000 tech crash (SEC data).

Compare outcomes:

- Single asset focus: Higher upside, catastrophic downside.

- Strategic allocation: Moderated gains, controlled losses.

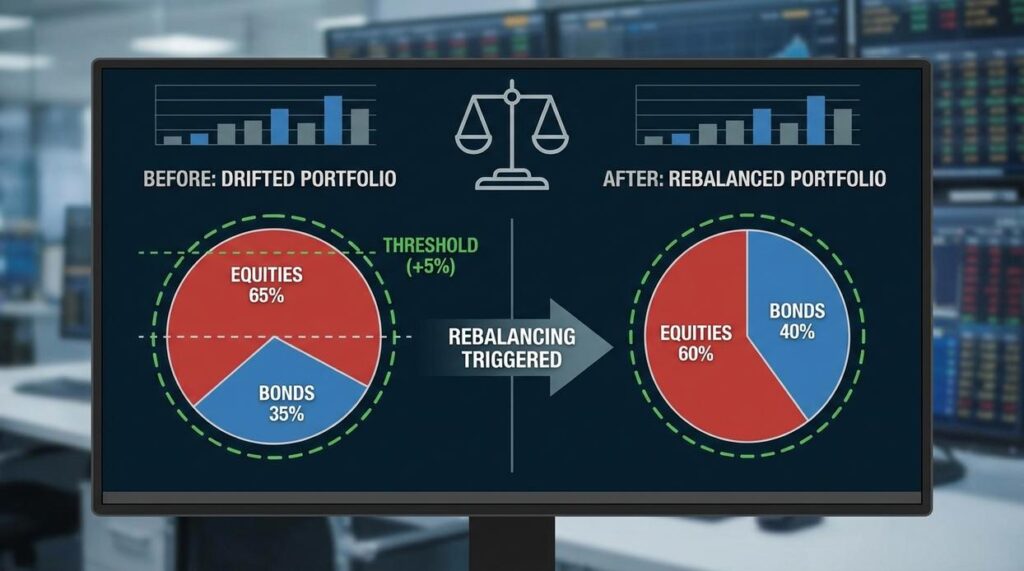

Pro tip: Rebalance annually to maintain target weights and prevent drift.

Diversification isn’t gambling less—it’s engineering endurance.

The Mechanics of Risk Reduction: Why Spreading Your Bets Works

At its heart, risk reduction depends on non-correlation, meaning assets that respond differently to the same economic shock. Investors often feel frustrated watching every holding drop at once, wondering why diversification “failed.” Usually, it did not; the mix simply was not balanced enough.

Think of a sports team: you need offense and defense. Growth stocks chase returns, while government bonds aim to steady the ship. When equities slide, high quality bonds have historically held value or risen, cushioning losses (like a reliable goalie during a playoff slump). According to Vanguard, portfolios blending stocks and bonds have shown lower volatility over decades than stocks alone.

Still, some argue concentration builds real wealth. True, big bets can outperform. Yet they also magnify drawdowns, which behavioral finance research shows investors struggle to endure (DALBAR reports many sell after losses).

So, instead, construct a diversified investment portfolio that includes:

- growth assets

- defensive assets

- alternative income sources

The goal is not perfection; it is smoother progress. Over time, reduced volatility supports compounding, lowers stress, and keeps you invested when headlines scream panic. Pro tip: rebalance annually to maintain alignment with your risk tolerance and goals.

Constructing Your Foundation: The Core Asset Classes

Building wealth without understanding asset classes is like assembling IKEA furniture without the manual—possible, but emotionally taxing.

A diversified investment portfolio stands on four primary pillars:

-

Equities (Stocks): The engine of growth. Stocks represent ownership in a company. Large-cap stocks are shares of established, financially stable firms (think household names). Small-cap stocks belong to smaller companies with higher growth potential—and yes, higher drama. Adding international stocks broadens exposure beyond your home market, capturing global expansion.

-

Fixed Income (Bonds): The stabilizer. A bond is essentially a loan you give to a government or corporation in exchange for interest payments. Government bonds are typically lower risk, while corporate bonds offer higher yields with added risk. Historically, bonds have often cushioned portfolios during equity downturns (Morningstar, 2023).

-

Real Assets (Real Estate & Commodities): Tangible investments that can hedge against inflation. Real estate may generate rental income, while commodities like gold have historically preserved purchasing power during volatile periods (World Gold Council, 2022). Think of them as the “serious adults” in the room.

-

Cash and Cash Equivalents: The liquidity layer. Cash, savings accounts, and money market funds provide flexibility and capital preservation. They may not be exciting (no one brags about their cash position at parties), but they allow you to act quickly when opportunities arise.

Of course, critics argue cash drags returns and bonds underperform stocks long term. Fair. But stability and optionality have value—especially during market chaos.

For a deeper breakdown, explore asset allocation strategies for different life stages.

Advanced Tactics: Leveraging Structure for Maximum Returns

Building a diversified investment portfolio is a solid start—but structure is where serious gains (and losses) are shaped.

Geographic and Sector Diversification

Think beyond stocks vs. bonds. If all your equities sit in U.S. tech, you’re not truly diversified. Spread exposure across:

- Regions: U.S., Europe, emerging Asia

- Sectors: Technology, healthcare, consumer staples, energy

- Economic drivers: Growth-focused vs. defensive industries

For example, when U.S. tech cooled in 2022, energy stocks outperformed as oil prices surged (U.S. Energy Information Administration). Geographic and sector balance cushions LOCALIZED SHOCKS.

The Role of Alternative Investments

Alternatives are assets outside traditional public markets—like private credit (direct lending to companies) or venture capital (early-stage business funding). They may provide non-correlated returns, meaning they don’t move in lockstep with stocks (Morningstar).

Practical approach:

- Limit allocation to 5–15% if you’re experienced

- Confirm liquidity timelines (some lock capital for years)

- Stress-test worst-case scenarios

Higher return potential? Yes. Higher risk and illiquidity? Also yes.

Strategic Use of Debt and Leverage

Leverage means investing with borrowed capital. If returns exceed borrowing costs, gains amplify. If not, losses multiply. Start small, model downside cases, and NEVER leverage speculative bets.

Integrating Liabilities

List all debts, interest rates, and maturities. Refinance high-interest obligations first. Align loan duration with investment horizon. True wealth planning balances assets AND liabilities—because structure determines resilience.

From Theory to Action: Building Your Diversified Future

An undiversified portfolio isn’t a strategy—it’s like sailing across the ocean in a single-engine boat and hoping the motor never fails. It might work for a while. Until it doesn’t.

A diversified investment portfolio, by contrast, is a fleet. Stocks act as your speedboats, built for growth. Bonds are the cargo ships, steady and dependable. Real assets—like real estate or commodities—are your anchors, adding stability when markets churn. When one vessel slows, another keeps you moving forward. That’s asset allocation: the intentional distribution of capital across different asset types to balance risk and return (Modern Portfolio Theory, Markowitz, 1952).

Critics argue diversification “dilutes” returns. Why not put everything into the highest performer? It’s a fair question. But concentration is like betting your entire harvest on a single crop—great in perfect weather, disastrous in a drought. History shows diversified portfolios have reduced volatility without eliminating growth potential (Brinson, Hood & Beebower, 1986).

Volatility isn’t the storm—it’s the waves. Managed correctly, waves are navigable.

Now it’s your move. Review your holdings. Measure your risk tolerance—the level of uncertainty you can endure without panic-selling. Adjust deliberately. Build structure. Because wealth, like architecture, stands longer when the foundation is thoughtfully engineered.

Build Momentum With the Right Leverage Strategy

You came here to better understand how leverage, debt structuring, and high-risk investment mechanics can accelerate wealth creation. Now you have a clearer view of how progress points, calculated risk, and strategic capital deployment work together to strengthen a diversified investment portfolio.

The real pain point isn’t lack of opportunity — it’s misusing leverage, overexposing capital, or structuring debt the wrong way. One poorly planned move can erase months or years of gains. But when leverage is aligned with your portfolio goals and risk tolerance, it becomes a powerful growth engine instead of a liability.

Your next step is simple: evaluate your current portfolio structure, identify where leverage can be optimized, and refine your debt strategy before your next capital move. Don’t let inefficient structuring limit your upside.

If you’re ready to reduce unnecessary risk while maximizing capital efficiency, take action now. Use proven leverage frameworks, stress-test your positions, and apply disciplined portfolio planning strategies that serious investors rely on. The difference between stalled growth and accelerated wealth is strategic execution — start optimizing today.

Maryan Bradleyankie writes the kind of wealth portfolio planning content that people actually send to each other. Not because it's flashy or controversial, but because it's the sort of thing where you read it and immediately think of three people who need to see it. Maryan has a talent for identifying the questions that a lot of people have but haven't quite figured out how to articulate yet — and then answering them properly.

They covers a lot of ground: Wealth Portfolio Planning, Expert Advice, High-Risk Investment Mechanics, and plenty of adjacent territory that doesn't always get treated with the same seriousness. The consistency across all of it is a certain kind of respect for the reader. Maryan doesn't assume people are stupid, and they doesn't assume they know everything either. They writes for someone who is genuinely trying to figure something out — because that's usually who's actually reading. That assumption shapes everything from how they structures an explanation to how much background they includes before getting to the point.

Beyond the practical stuff, there's something in Maryan's writing that reflects a real investment in the subject — not performed enthusiasm, but the kind of sustained interest that produces insight over time. They has been paying attention to wealth portfolio planning long enough that they notices things a more casual observer would miss. That depth shows up in the work in ways that are hard to fake.

Maryan Bradleyankie writes the kind of wealth portfolio planning content that people actually send to each other. Not because it's flashy or controversial, but because it's the sort of thing where you read it and immediately think of three people who need to see it. Maryan has a talent for identifying the questions that a lot of people have but haven't quite figured out how to articulate yet — and then answering them properly.

They covers a lot of ground: Wealth Portfolio Planning, Expert Advice, High-Risk Investment Mechanics, and plenty of adjacent territory that doesn't always get treated with the same seriousness. The consistency across all of it is a certain kind of respect for the reader. Maryan doesn't assume people are stupid, and they doesn't assume they know everything either. They writes for someone who is genuinely trying to figure something out — because that's usually who's actually reading. That assumption shapes everything from how they structures an explanation to how much background they includes before getting to the point.

Beyond the practical stuff, there's something in Maryan's writing that reflects a real investment in the subject — not performed enthusiasm, but the kind of sustained interest that produces insight over time. They has been paying attention to wealth portfolio planning long enough that they notices things a more casual observer would miss. That depth shows up in the work in ways that are hard to fake.