Markets are shifting faster than most investors can adapt—and if you’re here, you’re likely looking for clear, practical insight into leveraged finance, wealth portfolio planning, and the mechanics behind high-risk investment decisions. This article is built to meet that need directly. We break down how progress points in a financial journey influence capital allocation, how debt structuring techniques can amplify (or undermine) returns, and when leverage becomes a strategic advantage rather than a liability.

Many investors struggle not because they lack ambition, but because they lack a structured understanding of risk layering, cash flow timing, and portfolio rebalancing strategies that align with changing market conditions. Here, you’ll find data-driven analysis, scenario-based examples, and proven financial frameworks used in complex capital environments.

Our insights draw from extensive analysis of leveraged markets, risk modeling principles, and real-world capital structuring approaches—so you can make informed, calculated decisions instead of reactive ones.

Beyond ‘Set and Forget’: Mastering Dynamic Portfolio Rebalancing

“Set it and forget it” sounds comforting, but markets don’t stand still. Over time, price swings create portfolio drift—a gradual shift in your asset allocation away from its original targets. Consequently, you might carry more equity risk than intended after a bull run, or miss upside by clinging to excess cash.

Professional wealth managers treat rebalancing as disciplined risk control, not a routine chore. For example, threshold-based adjustments trigger trades when allocations drift beyond preset bands, while calendar-based reviews enforce quarterly or annual resets. These portfolio rebalancing strategies help lock in gains and systematically buy undervalued assets.

In practice, dynamic adjustments preserve your intended risk-return profile across volatile cycles, ensuring your capital works as designed, consistently aligned.

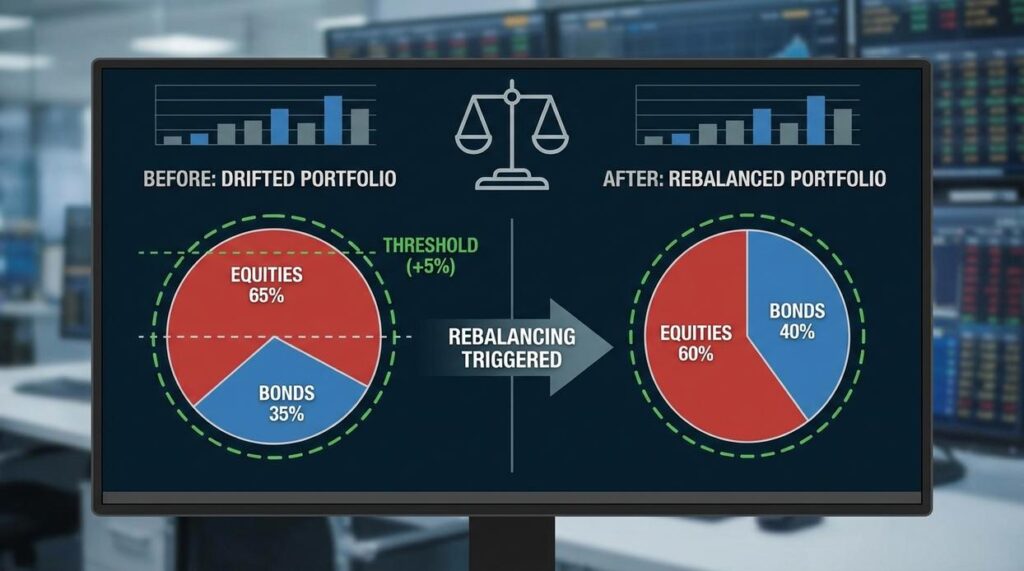

The Core Principle: Understanding Portfolio Drift and Risk Creep

Think of your portfolio like a perfectly balanced seesaw. At the start, a 60/40 stock-to-bond mix sits level—steady, intentional, built for a specific risk tolerance. Now imagine stocks surge during a strong market year. Suddenly, that 60/40 split quietly shifts to 70/30. Nothing feels dramatic, yet the balance has changed. This silent shift is portfolio drift—when market movements push your asset allocation away from its original target.

At first glance, you might shrug. After all, gains are good, right? However, here’s where risk creep enters. As stocks take up more space, your portfolio becomes more volatile. What once felt like a stable sedan now handles like a sports car on a wet road (thrilling, but less forgiving).

Some argue you should “let winners run.” Fair point. But without guardrails, concentration risk builds quietly. The goal of portfolio rebalancing strategies isn’t to chase higher returns—it’s to restore equilibrium. By trimming outperformers and adding to laggards, you systematically buy low and sell high, keeping emotion out of the driver’s seat.

Method 1: The Discipline of Calendar-Based Rebalancing

Calendar-based rebalancing is exactly what it sounds like: you review and adjust your investments on a fixed schedule—quarterly, semi-annually, or annually. In practice, that means comparing your current asset allocation (the percentage split between stocks, bonds, cash, etc.) to your target allocation, then buying or selling to realign.

At first, I ignored this structure. Instead, I rebalanced “when it felt right.” That was a mistake. I let winning positions run too long and hesitated to trim them (because selling winners feels wrong). Eventually, my risk exposure drifted far beyond my comfort zone.

Annual rebalancing is simple and often more tax-efficient, since fewer trades can mean fewer taxable events. On the other hand, quarterly reviews allow faster corrections during volatile markets—but transaction costs and overtrading can creep in. Therefore, your frequency should reflect both discipline and cost awareness.

More advanced investors align rebalancing with year-end tax-loss harvesting—selling underperforming assets to offset capital gains (IRS guidelines permit this with specific rules).

This approach works best for long-term investors who want structured, low-maintenance portfolio rebalancing strategies. Sometimes boring really does win (just ask any index fund devotee).

Method 2: The Precision of Threshold-Based Rebalancing

Threshold-based rebalancing is, in my view, where discipline meets common sense. Instead of rebalancing on a fixed date, you set percentage “corridors” around your target allocations. For example, if your portfolio holds 60% equities and 40% bonds, you might allow a 5% band. If equities rise to 66%, crossing the upper limit, you rebalance. If they stay within 55%–65%, you leave it alone.

That’s the entire mechanism: act only when allocations drift beyond predefined limits. It’s one of the more practical portfolio rebalancing strategies because it filters out noise (and markets generate plenty of it).

Now, setting intelligent thresholds is where judgment comes in. Wider bands, like 10%, reduce transaction costs and taxes but allow more drift. Narrower bands, like 5%, tighten risk control yet can increase trading expenses. Personally, I favor slightly wider bands for taxable accounts—especially after reviewing tax efficient portfolio planning techniques explained.

Here’s why this method shines: volatility. During major swings—think 2008 or the early 2020 pandemic shock—assets can move fast. Thresholds force action when risk meaningfully changes, not when a calendar reminder pops up.

Some argue calendar rebalancing is simpler. True. But simplicity isn’t always precision. If you want a system that reacts to market dynamics without daily micromanagement, this approach strikes a smart balance.

Advanced investors know rebalancing isn’t just about selling winners. It’s about using cash intelligently. When new capital comes in, I prefer directing it toward underweight asset classes instead of trimming outperformers. That simple shift reduces transaction costs and, frankly, emotional decision-making. Likewise, withdrawals can be pulled from overweight positions to quietly restore balance.

Tax-aware rebalancing is non-negotiable in my view. Adjust inside tax-advantaged accounts like 401(k)s or IRAs first to avoid capital gains taxes, which the IRS confirms can materially reduce net returns (IRS.gov).

Meanwhile, dividends and interest shouldn’t sit idle. I like automatically reinvesting income into the most underweight sleeve—continuous, almost invisible portfolio rebalancing strategies at work.

For sophisticated investors, derivatives offer another layer. Options or futures can synthetically adjust exposure without selling core holdings, though this requires serious expertise and risk controls.

I’ll admit, some argue this overcomplicates a long-term plan. Fair point. But in volatile markets—think 2020-level swings—precision often beats passivity. Pro tip: automate what you can, and reserve complexity for when the payoff justifies it. Discipline compounds more reliably than brilliance.

Building a Resilient and Responsive Investment Strategy

To recap, you have three core tools: calendar rebalancing (adjusting at set intervals like quarterly), threshold rebalancing (acting when allocations drift beyond a set percentage), and cash-flow based rebalancing (using new contributions or withdrawals to realign holdings). Together, these portfolio rebalancing strategies form a flexible toolkit for the modern investor.

Now, I’ll admit—no single method is universally “best.” Markets shift, correlations break, and even well-tested rules can feel uncertain in extreme conditions. Still, the purpose isn’t perfection. It’s disciplined risk management.

In other words, rebalancing keeps your portfolio aligned with your goals, not your emotions (which, let’s be honest, can be unreliable).

So, take a moment. Do you actually have a rebalancing plan? If not, choose a method and implement it. Your future wealth may depend on it.

Take Control of Your Leverage Before It Controls You

You came here to better understand how leverage, debt structuring, and high-risk investment mechanics can either accelerate your wealth—or quietly erode it. Now you have a clearer view of how progress points, disciplined allocation, and portfolio rebalancing strategies work together to reduce volatility while preserving upside potential.

The reality is this: unmanaged leverage amplifies mistakes just as quickly as it multiplies gains. Without a structured approach, small miscalculations in debt exposure or asset weighting can compound into serious financial setbacks. That’s the pain most investors feel—uncertainty about whether their current structure can withstand market stress.

The solution is deliberate leverage management, strategic allocation, and consistent recalibration. When you align risk tolerance with calculated debt structuring and apply disciplined portfolio rebalancing strategies, you shift from reactive decision-making to controlled growth.

Now it’s time to act. Review your current leverage ratios, reassess your exposure to high-risk positions, and implement a structured rebalancing plan. If you’re serious about protecting your capital while positioning for aggressive upside, take the next step and get expert-backed guidance today. The right structure doesn’t just grow wealth—it protects it. Start optimizing now.

Gary Cuadradovona writes the kind of progress points content that people actually send to each other. Not because it's flashy or controversial, but because it's the sort of thing where you read it and immediately think of three people who need to see it. Gary has a talent for identifying the questions that a lot of people have but haven't quite figured out how to articulate yet — and then answering them properly.

They covers a lot of ground: Progress Points, Debt Structuring Techniques, Wealth Portfolio Planning, and plenty of adjacent territory that doesn't always get treated with the same seriousness. The consistency across all of it is a certain kind of respect for the reader. Gary doesn't assume people are stupid, and they doesn't assume they know everything either. They writes for someone who is genuinely trying to figure something out — because that's usually who's actually reading. That assumption shapes everything from how they structures an explanation to how much background they includes before getting to the point.

Beyond the practical stuff, there's something in Gary's writing that reflects a real investment in the subject — not performed enthusiasm, but the kind of sustained interest that produces insight over time. They has been paying attention to progress points long enough that they notices things a more casual observer would miss. That depth shows up in the work in ways that are hard to fake.

Gary Cuadradovona writes the kind of progress points content that people actually send to each other. Not because it's flashy or controversial, but because it's the sort of thing where you read it and immediately think of three people who need to see it. Gary has a talent for identifying the questions that a lot of people have but haven't quite figured out how to articulate yet — and then answering them properly.

They covers a lot of ground: Progress Points, Debt Structuring Techniques, Wealth Portfolio Planning, and plenty of adjacent territory that doesn't always get treated with the same seriousness. The consistency across all of it is a certain kind of respect for the reader. Gary doesn't assume people are stupid, and they doesn't assume they know everything either. They writes for someone who is genuinely trying to figure something out — because that's usually who's actually reading. That assumption shapes everything from how they structures an explanation to how much background they includes before getting to the point.

Beyond the practical stuff, there's something in Gary's writing that reflects a real investment in the subject — not performed enthusiasm, but the kind of sustained interest that produces insight over time. They has been paying attention to progress points long enough that they notices things a more casual observer would miss. That depth shows up in the work in ways that are hard to fake.