Understanding the leveraged buyout process is essential for investors, executives, and finance professionals looking to navigate high-stakes acquisitions with confidence. Whether you’re exploring private equity strategies, evaluating debt-heavy transactions, or assessing the risks behind acquisition financing, this article is designed to clarify how leveraged buyouts actually work in practice.

Many investors are drawn to the upside potential of leveraged transactions but struggle to grasp the mechanics behind capital structuring, debt layering, cash flow modeling, and risk allocation. Without a clear framework, it’s easy to underestimate the financial and operational pressures involved.

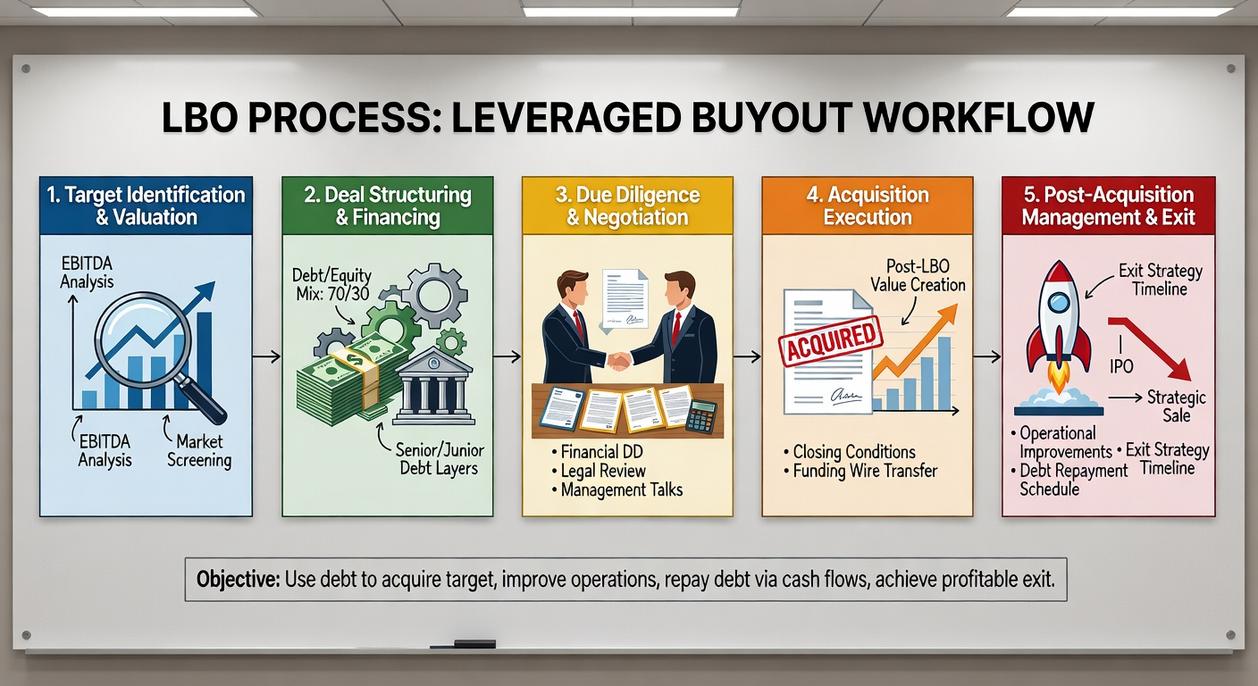

In this guide, we break down each stage of the leveraged buyout process, from target identification and valuation to financing structures and exit strategies. The insights presented are grounded in real-world leveraged finance analysis, portfolio structuring experience, and proven debt modeling techniques—giving you a practical, strategic understanding rather than just theory.

Growth through acquisition doesn’t require vast cash reserves; it requires disciplined debt strategy. A leveraged buyout lets you control a larger, established company by using borrowed funds backed by its own cash flow. The critical rule: the business must consistently generate enough free cash flow to service principal and interest. Ignore this, and risk compounds fast.

Follow the leveraged buyout process with precision:

• Target companies with predictable earnings and low capital expenditure needs.

• Structure debt with realistic covenants and conservative projections.

Pro tip: stress-test revenue under worst-case scenarios before signing. Prioritize liquidity over aggressive expansion assumptions at closing.

Phase 1: Identifying and Vetting the Ideal Acquisition Target

The first step in any successful deal is clarity. Before reviewing teasers or calling brokers, define your investment thesis—the core belief driving your acquisition. Which industry aligns with your expertise? What inefficiencies can you fix? What value can you uniquely add as an owner? Clear criteria prevent emotional decisions (and yes, shiny revenue numbers can be distracting).

A strong candidate in the leveraged buyout process typically shares several traits lenders trust and investors favor:

- Stable and predictable cash flows that support debt repayment

- Defensible market position, such as recurring contracts or brand loyalty

- Tangible assets that can serve as collateral

- Capable management team or a clear leadership transition plan

- Operational upside, including cost reductions or pricing improvements

Once criteria are set, build a focused pipeline. Use industry databases, broker relationships, and direct outreach to owners. Keep communication discreet and professional—confidentiality protects both sides. Prepare a concise introduction outlining your acquisition intent and financial capacity.

Pro tip: Create a simple scoring model to rank opportunities objectively. It reduces bias and helps you move quickly when the right deal appears.

Phase 2: The Critical Due Diligence and Valuation Process

Phase 2 is where deals either earn conviction—or quietly fall apart. In the leveraged buyout process, this is the point where assumptions meet evidence.

Beyond the Numbers (Financial Diligence)

Financial diligence means examining historical financial statements to test the quality of earnings—a term that refers to how sustainable and recurring profits truly are. Adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is often used to measure debt serviceability because lenders focus on predictable cash flow (Harvard Business Review, 2020).

Scrutinize:

- Revenue consistency and customer churn

- Working capital needs (inventory, receivables, payables)

- Existing debt terms and covenants

Some argue EBITDA is overused and ignores capital expenditures. That criticism is valid. But in leveraged transactions, EBITDA remains a practical proxy for repayment capacity—provided you also stress-test free cash flow.

Pro tip: Model downside cases with a 10–20% revenue drop to see if the company can still meet interest obligations.

Operational and Commercial Diligence

Assess customer concentration (no single client should dominate revenue), supply chain fragility, and competitive positioning. A company dependent on one supplier or one “hero” client may look strong—until that relationship changes (think of how quickly tech suppliers pivot under pressure).

Legal and Regulatory Diligence

Review contracts, pending litigation, compliance history, and regulatory exposure. Hidden liabilities can erode equity value overnight.

Valuation in a Leveraged Context

Use discounted cash flow (DCF)—which estimates value based on projected future cash flows—and comparable company analysis. The key question isn’t just “What is it worth?” but “How much debt can it safely support?” Sustainable leverage—not maximum leverage—drives durable returns.

Phase 3: Architecting the Deal and Securing Financing

If Phase 2 is about choosing the house, Phase 3 is about designing the mortgage—except the house costs millions and the mortgage has layers like a wedding cake at a royal ceremony.

Understanding the Capital Stack

Think of the capital stack as a pyramid. The base is the widest and most stable; the top is thinner but riskier.

- Senior Debt – The foundation. This is the largest, cheapest capital layer, typically provided by banks and secured by company assets. Because it sits first in line for repayment, it carries the lowest interest rate (safety has its privileges).

- Mezzanine Financing / Subordinated Debt – The middle layer. A hybrid of debt and equity, it fills the gap between senior debt and equity. It costs more but offers flexibility—like a financial shock absorber.

- Seller Financing – Here, the seller acts like a temporary banker, carrying part of the purchase price as a loan. This can signal confidence in the business’s future.

- Equity Contribution – The acquirer’s cash, usually 20–40% of the purchase price. This is the skin in the game.

Negotiating the Term Sheet

A term sheet is the blueprint. It outlines interest rates, covenants (rules borrowers must follow), and repayment schedules. Securing commitment letters from lenders locks in these terms before closing. Miss a covenant, and consequences can escalate FAST.

The Art of Structuring

Balancing these layers is like tuning a race car engine: more leverage boosts returns, but too much increases breakdown risk. Critics argue heavy debt magnifies failure odds—and they’re not wrong. The risk and return dynamics in leveraged lending prove that higher leverage amplifies both gains and losses.

Within the leveraged buyout process, precision matters. Structure wisely, and returns compound. Overreach, and the pyramid wobbles.

The closing process finalizes legal documentation, funds the deal, and transfers ownership to new hands. In the leveraged buyout process, this is where strategy becomes reality and risk turns into opportunity. The benefit? Certainty, control, and the power to execute.

The first 100 days demand a clear integration plan—aligning teams, systems, and costs to unlock synergies, meaning combined value greater than separate parts. (Yes, like assembling the Avengers.) Momentum here compounds fast.

Managing debt requires disciplined cash flow oversight—tracking inflows, obligations, and covenants to avoid default. Pro tip: prioritize liquidity buffers before expansion. Do this well, and equity value accelerates.

From Leverage to Long-Term Value Creation

Recapping the core process, the four phases are: 1. Target Identification, 2. Diligence, 3. Structuring, and 4. Integration. However, closing the deal is only the starting line. The real objective is to strengthen operations, pay down debt, and expand equity value.

To do that, follow this guidance: 1. Choose cash-flow-stable businesses. 2. Stress-test assumptions relentlessly. 3. Structure debt conservatively. 4. Execute integration with measurable milestones.

In other words, treat the leveraged buyout process as a disciplined system, not a gamble. Ultimately, borrowed capital magnifies returns only when planning, analysis, and execution remain rigorous consistently.

Understanding the intricacies of leveraged buyouts can significantly enhance your investment strategy, but avoiding common pitfalls that slow down measurable progress is equally crucial for success in the world of finance – for more details, check out our Common Mistakes That Slow Down Measurable Progress.

Mastering the Leveraged Buyout Landscape

You came here to understand how the leveraged buyout process really works — from capital stacking and debt structuring to risk allocation and value creation. Now you have a clearer picture of how strategic leverage, disciplined underwriting, and precise execution can turn complex deals into calculated opportunities.

The reality is that leveraged transactions amplify both upside and risk. Misjudging cash flow durability, covenant structures, or exit timing can erode returns quickly. But when structured correctly, leverage becomes a powerful wealth acceleration tool — not a liability.

The next move is yours.

If you’re serious about executing smarter deals, optimizing your capital stack, or stress-testing your portfolio against downside risk, take action now. Explore advanced structuring strategies, refine your due diligence framework, and align every deal with a clear risk-adjusted return target.

Don’t let uncertainty stall your momentum. Get the insights, tools, and frameworks trusted by high-level investors to navigate complex leveraged transactions with confidence. Strengthen your strategy today and position your next deal for disciplined, high-performance growth.

Maryan Bradleyankie writes the kind of wealth portfolio planning content that people actually send to each other. Not because it's flashy or controversial, but because it's the sort of thing where you read it and immediately think of three people who need to see it. Maryan has a talent for identifying the questions that a lot of people have but haven't quite figured out how to articulate yet — and then answering them properly.

They covers a lot of ground: Wealth Portfolio Planning, Expert Advice, High-Risk Investment Mechanics, and plenty of adjacent territory that doesn't always get treated with the same seriousness. The consistency across all of it is a certain kind of respect for the reader. Maryan doesn't assume people are stupid, and they doesn't assume they know everything either. They writes for someone who is genuinely trying to figure something out — because that's usually who's actually reading. That assumption shapes everything from how they structures an explanation to how much background they includes before getting to the point.

Beyond the practical stuff, there's something in Maryan's writing that reflects a real investment in the subject — not performed enthusiasm, but the kind of sustained interest that produces insight over time. They has been paying attention to wealth portfolio planning long enough that they notices things a more casual observer would miss. That depth shows up in the work in ways that are hard to fake.

Maryan Bradleyankie writes the kind of wealth portfolio planning content that people actually send to each other. Not because it's flashy or controversial, but because it's the sort of thing where you read it and immediately think of three people who need to see it. Maryan has a talent for identifying the questions that a lot of people have but haven't quite figured out how to articulate yet — and then answering them properly.

They covers a lot of ground: Wealth Portfolio Planning, Expert Advice, High-Risk Investment Mechanics, and plenty of adjacent territory that doesn't always get treated with the same seriousness. The consistency across all of it is a certain kind of respect for the reader. Maryan doesn't assume people are stupid, and they doesn't assume they know everything either. They writes for someone who is genuinely trying to figure something out — because that's usually who's actually reading. That assumption shapes everything from how they structures an explanation to how much background they includes before getting to the point.

Beyond the practical stuff, there's something in Maryan's writing that reflects a real investment in the subject — not performed enthusiasm, but the kind of sustained interest that produces insight over time. They has been paying attention to wealth portfolio planning long enough that they notices things a more casual observer would miss. That depth shows up in the work in ways that are hard to fake.